Surfing the Hardware Wave

Why the incoming physical renaissance is the most exciting frontier to build, fund, and navigate

As technology pushed into new digital frontiers, the venture ecosystem effectively abandoned its industrial roots. While heavy manufacturing never stopped, it lost its appeal; building software was simply seen as the smarter, cooler career path for ambitious entrepreneurs. But that cycle is breaking. With the digital world being optimized faster than ever, founders are turning their attention back to the physical bottlenecks we used to accept. We are entering a physical-world startup wave, and it is being accelerated by a single force: what the PayPal Mafia did for SaaS, SpaceX is about to do for industrial hardware.

The Gravity of Legacies

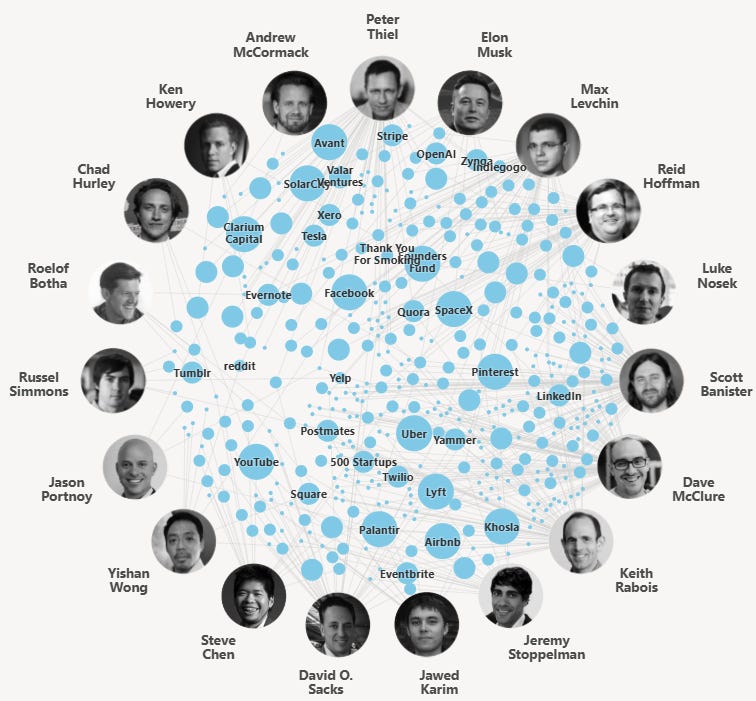

In the middle of the early 2000s dot-com bust, eBay bought PayPal. At the time, it looked like a simple move to integrate commerce and payments. In reality, it was the genesis of the modern web and SaaS era. The PayPal exit flooded a tight network of operators with capital right when traditional funding was frozen. They used that money to build their own companies or fund the startups of their former colleagues. By the time Fortune published its famous piece naming the PayPal Mafia five years later, the infrastructure for the next generation of tech giants was already locked in place.

When you look at the visual web of those investments, it becomes clear that exits of this magnitude generate a self-sustaining ecosystem. The most successful companies act as an operational school, when the exit arrives, the alumni graduate with a shared execution playbook and a wealthy support network to back ideas that traditional VCs might find too complicated.

Today, the next big exit is nearer than ever, and the infrastructure is already fully built. Organized alumni websites and investment syndicates prove that the SpaceX network is not a loose group of friends, but a highly structured capital machine. SpaceX’s liquidity event is poised to be the exact same catalyst for weird, heavy, and physical startups that PayPal was for the internet.

The Training Ground

In the early days of industrial development, fast-scaling companies had two options when they needed a specific component: they could either ask an employee to spin out a dedicated company, or they could vertically integrate the process themselves. Ford’s legendary success, for example, was built on a highly vertically integrated model that ultimately caused the entire Detroit area to develop around serving that one industry. This happened because they were building an entirely new sector; existing solutions simply couldn’t meet their requirements for quality and delivery times, meaning everything had to be built in-house or right across the street (more on ConteNido). Therefore, innovation has always clustered around its constraints, when no supplier exists, the founder becomes one, and the ecosystem builds itself outward from that pure necessity.

With the expansion of globalization, outsourcing became the default industry strategy. However, recent supply chain crises and a lack of manufacturing resilience are forcing companies to return to tightly clustered industrial ecosystems. Inside these frontiers, engineers are identifying massive supply chain gaps and exiting to build the solutions themselves backed directly by their ex-employers and colleagues. Today, the fastest way to solve a supply chain gap is for an internal spin out and build the solution themselves.

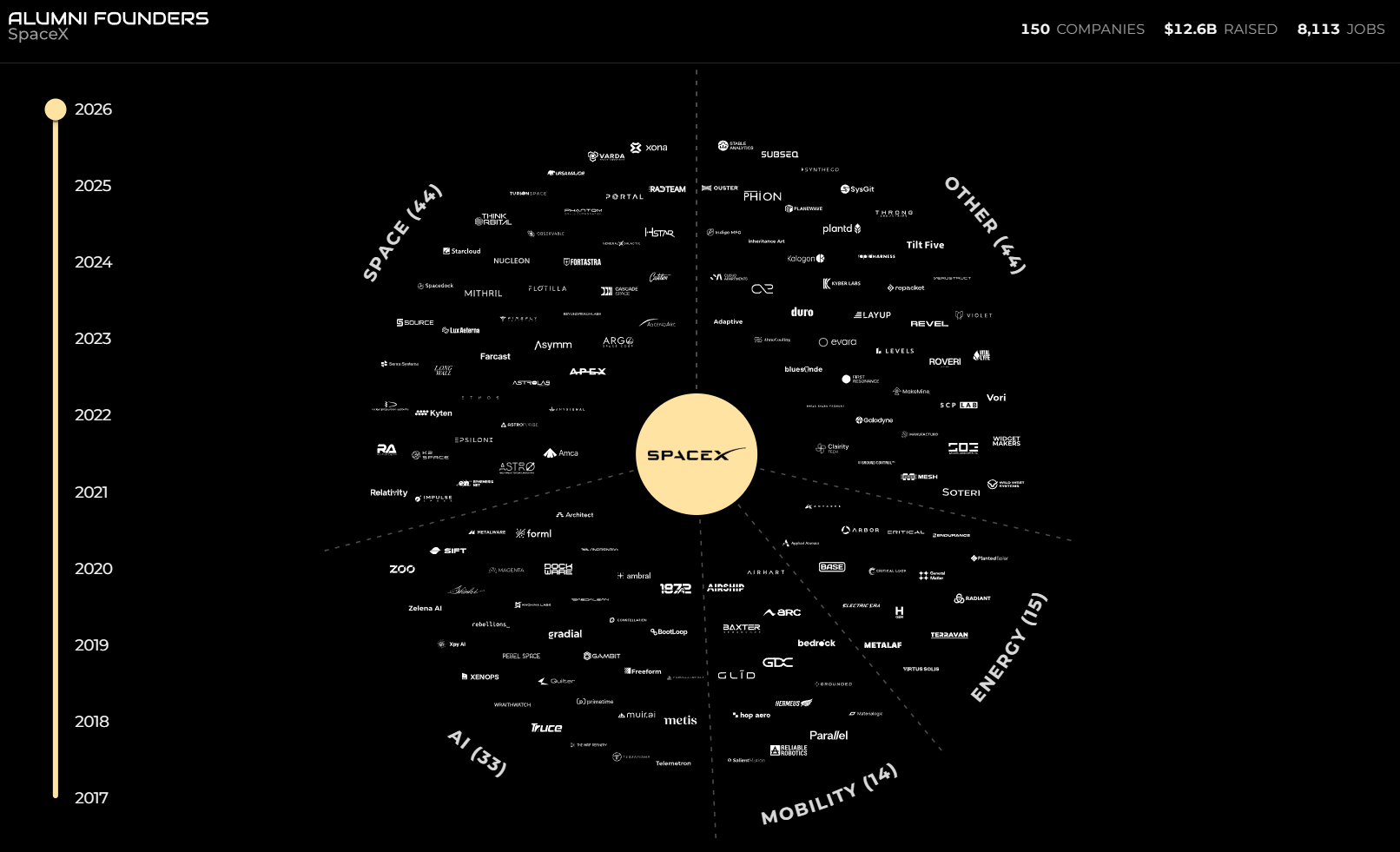

This is exactly what is happening with SpaceX. When they started, the commercial space industry was essentially non-existent; apart from Iridium’s 1999 bankruptcy, no one was tackling the space frontier and its projected $4.3 trillion TAM (as of 2024). With no established supply chain to call, SpaceX had the same two historical choices: either build everything in-house, or watch team members exit to build the missing pieces themselves, funded by the network they came from. The result is a completely self-replicating industrial ecosystem, evidenced by the 44 space-focused startups already founded by ex-SpaceX employees.

The collision of these two forces is exactly what makes this moment unprecedented. The fragility of global supply chains is forcing the market to demand localized, resilient industrial clusters. But you cannot simply build a new manufacturing ecosystem into existence, you need operators and engineers who actually know how to build the underlying infrastructure from scratch. This is why the extreme vertical integration of frontier giants is the missing puzzle piece. By forcing their teams to solve every physical bottleneck in-house, companies like SpaceX haven’t just been building rocketships; they have been running effective training grounds for the exact type of talent required to build new industries. The supply chain crisis created the massive market necessity, and these newly trained, highly technical alumni networks are providing the execution.

The Shift

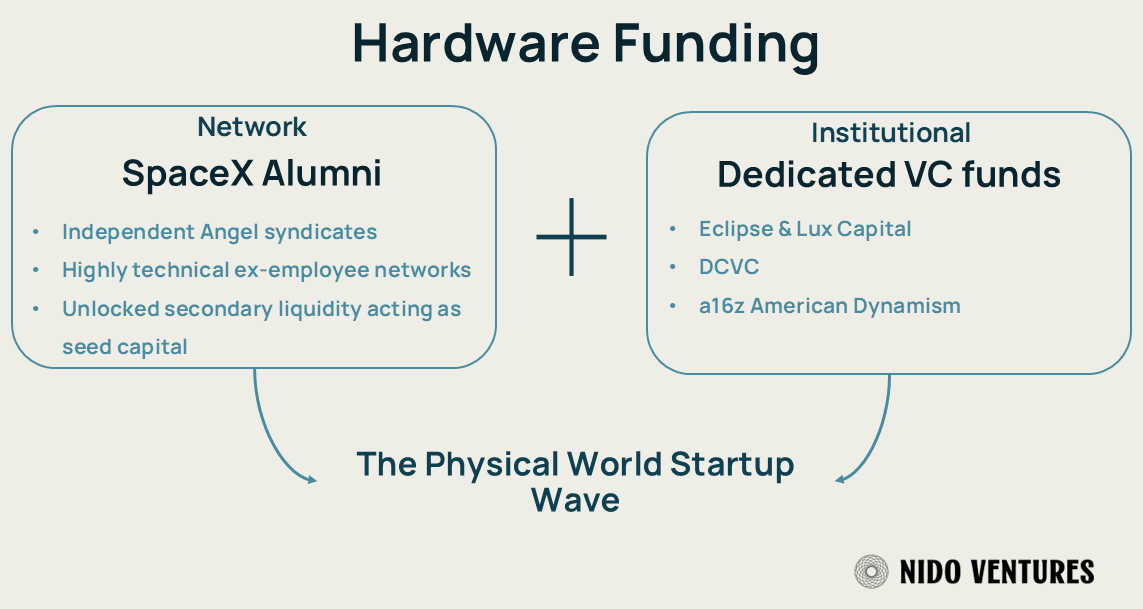

Engineers are finding new ways to bypass traditional funding paths. Early SpaceX employees who have already cashed out through secondary liquidity events are acting as angel investors for the next generation. This proves that a massive capital flywheel is spinning entirely independently of traditional VC constraints. The same flywheel that built the early 2000s software platform is spinning up for hardware today, fueled by a dual engine: a tight network of ex-SpaceX operators acting as alternative seed capital, moving in parallel with institutions raising massive deep-tech vehicles.

Another major shift is being driven by the AI boom. Historically, engineers trying to build physical companies had to either join legacy incumbents or pitch highly technical ideas that were at a severe disadvantage when compared to high-margin digital SaaS startups. But the constant infrastructure gaps exposed by AI (more in ConteNido) have changed the old norm.

Furthermore, as frontier AI models require increasingly expensive compute, software margins are narrowing. The sheer capital needed to compete against big tech is persuading both investors and founders to look at physical, hardware-based approaches they previously would have ignored. Some of the most interesting businesses today look more like infrastructure developers than software companies. Crusoe began by using flared gas to run crypto miners, but now operates as a vertically integrated AI platform, designing high‑density GPU campuses and 100 MW on‑site power plants.

Ultimately, SpaceX has trained a highly efficient pool of engineers who have a deep understanding of the physical constraints that standard software founders simply do not possess. This makes it significantly easier for them to exit the company and successfully execute these highly complex, infrastructure-grade products.

The Signs

The exits have already started. Quietly, a first wave of SpaceX alumni has been leaving to build companies that look nothing like the venture-backed SaaS playbook. Instead, they are applying the vertically integrated, constraint-solving model they learned on the job. The sectors they are choosing aren’t random; they cluster strictly around the heaviest physical bottlenecks: energy, fabrication, mobility, and infrastructure.

Starlink set the precedent for this movement. It proved that a service historically requiring massive, centralized infrastructure (like global telecoms) could be compressed, democratized, and deployed at scale. SpaceX alumni are taking this exact framework into “stranded” niches waiting to be disrupted. They are abandoning the software playbook, opting instead for a rapid, hardware-in-the-loop iteration model-building complex systems in the lab and solving physical bottlenecks in real-time.

When mapping the distribution of these new startups, a clear pattern emerges. While a significant portion remains in the aerospace sector, overlapping or building on top of SpaceX’s domain, the concentration is rapidly expanding into AI hardware, mobility, and energy grids.

When looking into the distribution of existing SpaceX alumni startups, we see that most of them stay in the space sector where they are either overlapping with SpaceX’s domain or building on top of it. With AI, mobility, and energy as the other sectors with more concentration.

Looking at this selected list, it is clear that they are not building in isolated sectors. They are executing three distinct industrial playbooks aimed at overcoming physical constraints:

Decentralizing Infrastructure: Bypassing massive, slow-moving utility projects by shrinking heavy infrastructure into portable, distributed nodes.

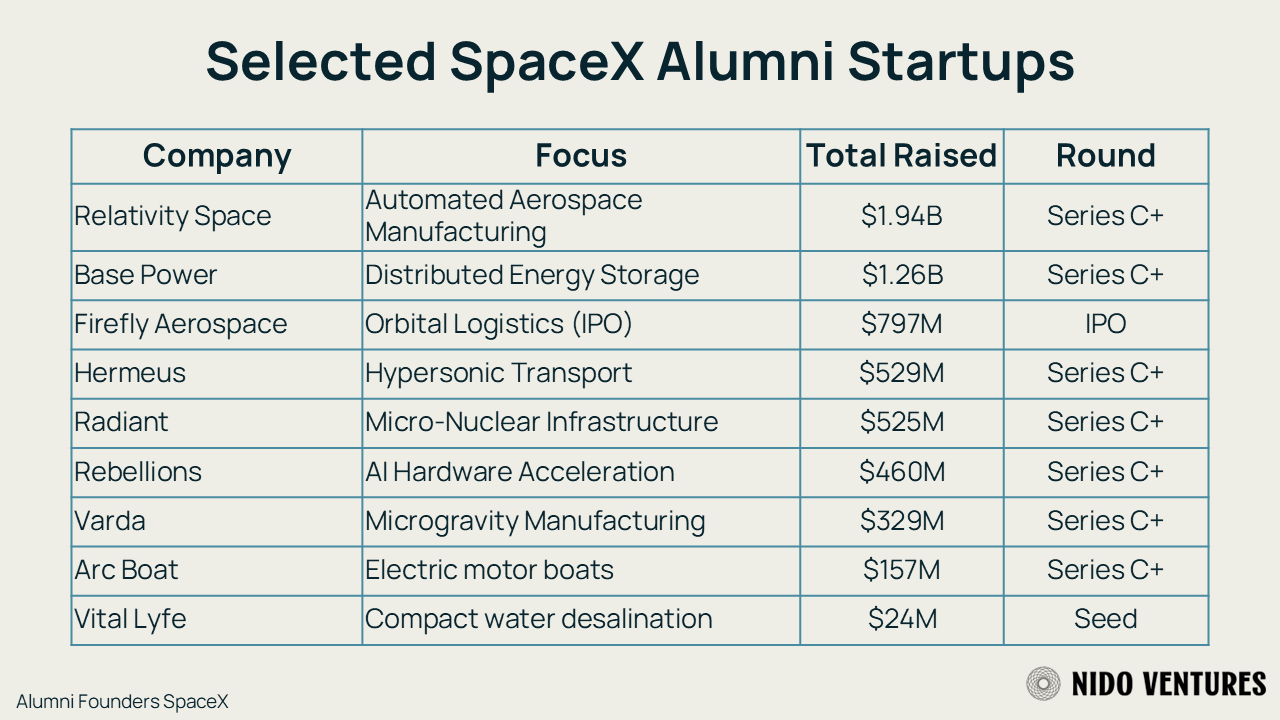

Base Power, Radiant and Vital Lyfe.

The global grid for power and water is a massive bottleneck. Rather than building multi-billion-dollar centralized plants, these founders are democratizing industrial-grade resource generation and pushing it directly to the edge of the network.

Next-Gen Fabrication & Compute: Radically altering how and where complex products are assembled, moving away from fragmented supply chains into highly automated or novel environments.

Relativity Space, Varda and Rebellions.

Whether it is leveraging microgravity to formulate pharmaceuticals, using massive robotic arms to print rocket fuselages, or fabricating the specialized silicon required for the AI boom, these companies are completely restructuring industrial production.

Extreme Mobility & Logistics: Eradicating the friction and carbon footprint of moving heavy payloads across water, air, and orbit.

Hermeus, FireFly Aerospace and Arc Boat.

Moving matter efficiently is the ultimate physical constraint. By applying rapid, software-like iteration cycles to everything from orbital launch vehicles to electrified marine transport, these companies are making next-generation logistics commercially viable.

It is not a coincidence that these startups are clustering in sectors that have seen virtually no disruption in the last few decades. Previous generations of founders accepted legacy infrastructure as an unmovable object; this new wave views it as a challenge to be engineered away. Take Vital Lyfe, for example. Instead of accepting the massive infrastructure traditionally required for water desalination, they built a compact, portable desalination “crate.” This single piece of hardware opens entirely new geographic frontiers where the lack of freshwater was previously the ultimate restriction.

The Surf

The momentum generated by this core group of alumni is already spilling over. A broader class of founders has recognized the precedent: the ultimate venture-scale opportunities left to solve are entirely physical. Armed with modern software to drive unprecedented productivity, the manufacturing and industrial infrastructure is moving faster than before. Ideas that were previously written off as too capital intensive or constrained by legacy supply chains, like modular desalination crates or autonomous underwater exploration drones, are now highly scalable targets. They just need the right engineers to execute them.

This shift in the broader narrative is heavily anchored by SpaceX’s recent merger with xAI. By bridging the world’s most aggressive physical manufacturing ecosystem with elite AI researchers, they are supercharging the talent pool through shared problem-solving. They are inadvertently training a pool for both industrial execution and frontier compute, ensuring this incoming wave of hardware is natively integrated with AI.

All of this is building toward a historic breaking point. SpaceX is reported to be targeting an imminent IPO with a staggering valuation north of $1.5 trillion. When that liquidity event officially hits the public markets, it will permanently destroy the legacy VC argument that “hardware is too hard”. It will let loose a wave of unconstrained capital and highly trained operators into the ecosystem. What the PayPal exit did for the internet in 2002, the SpaceX IPO is about to do for the physical world. The wave is already forming; the only question is who’s going to surf it.