Versión en español aquí

In the world of venture capital, some of the most influential players aren’t the ones founding startups or writing term sheets — they’re the university endowments and foundations quietly supplying the capital behind the scenes. In the United States, endowments from schools like Yale, Harvard, and Stanford have become some of the most influential limited partners (LPs) in venture funds, often committing hundreds of millions across multiple fund cycles (PitchBook). Their long-term horizons, permanent capital, and appetite for innovation make them the kind of investors General Partners (GPs) dream of having.

But in Latin America, the story looks very different. The capital is there, often sitting in traditional stock and bond portfolios or locked inside private banks, but the model of professional, diversified endowment investing hasn’t taken root (more on ANDE Global). This gap matters, not only because it limits the flow of capital into startups, but also because it leaves many wealthy institutions and families without the compounding power that U.S. endowments have enjoyed for decades.

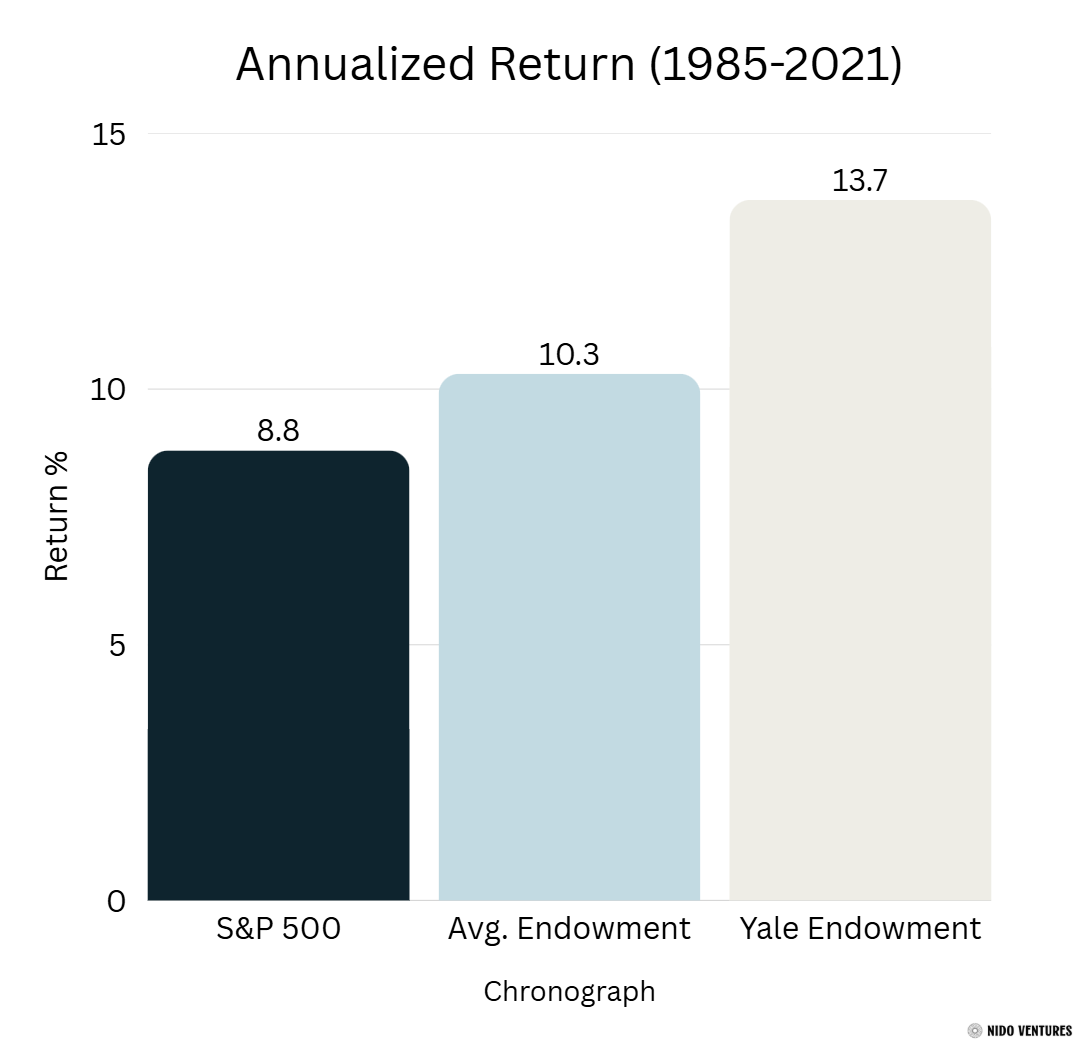

Figure 1: Long-Term Outperformance of Yale’s Endowment

That contrast is what drew me to explore the subject more deeply. Earlier this summer, while in Guatemala, I attended a talk where the role of U.S. endowments in venture capital was briefly highlighted. The slide showing their influence over the venture ecosystem sparked my curiosity: how do these funds work, why have they been so successful, and could something similar emerge in Latin America?

To answer those questions, I spoke with Wendy Li, co-founder of Ivy Invest, and Ana Carolina (Caro) Mexia, one of the GPs at Nido Ventures. Wendy spent nearly two decades managing money for endowments and foundations, including the Metropolitan Museum of Art in New York, before launching Ivy Invest to bring “endowment-style” investing to individuals. That conversation provided a behind-the-scenes look at how endowments think, the challenges they face today, and what lessons might matter for investors and institutions in our region.

What Are Endowments and Why Do They Matter?

Endowments are investment funds created by universities, foundations, and cultural institutions to provide long-term financial stability. In the U.S., they collectively manage over $840 billion (more on NACUBO), making them one of the most influential investor groups in the world. Unlike pensions or hedge funds, endowments are “permanent capital”, designed to last in perpetuity, which allows them to tolerate illiquidity and pursue higher returns.

This approach, popularized by Yale’s David Swensen, became known as the “Yale Model.” Instead of sticking to a 60/40 mix of stocks and bonds, Yale and peers shifted heavily into private markets like venture capital, private equity, hedge funds, and real assets. Over time, this strategy consistently outperformed traditional portfolios and turned endowments into anchor LPs for top VC funds. Over 36 years, that strategy grew Yale’s endowment from $1.3 billion to over $40 billion, with annualized gains that outperformed peers by several percentage points.

This wasn’t just about picking sectors or riding waves. Swensen, together with Dean Takahashi, placed enormous importance on manager selection—the skill and network to identify and access the best funds. In fact, Yale calculates that just 40% of the endowment’s “alpha” came from asset allocation; the other 60% was thanks to picking the right managers. That’s a level of diligence and inside access few institutions can match (more on Chronograph).

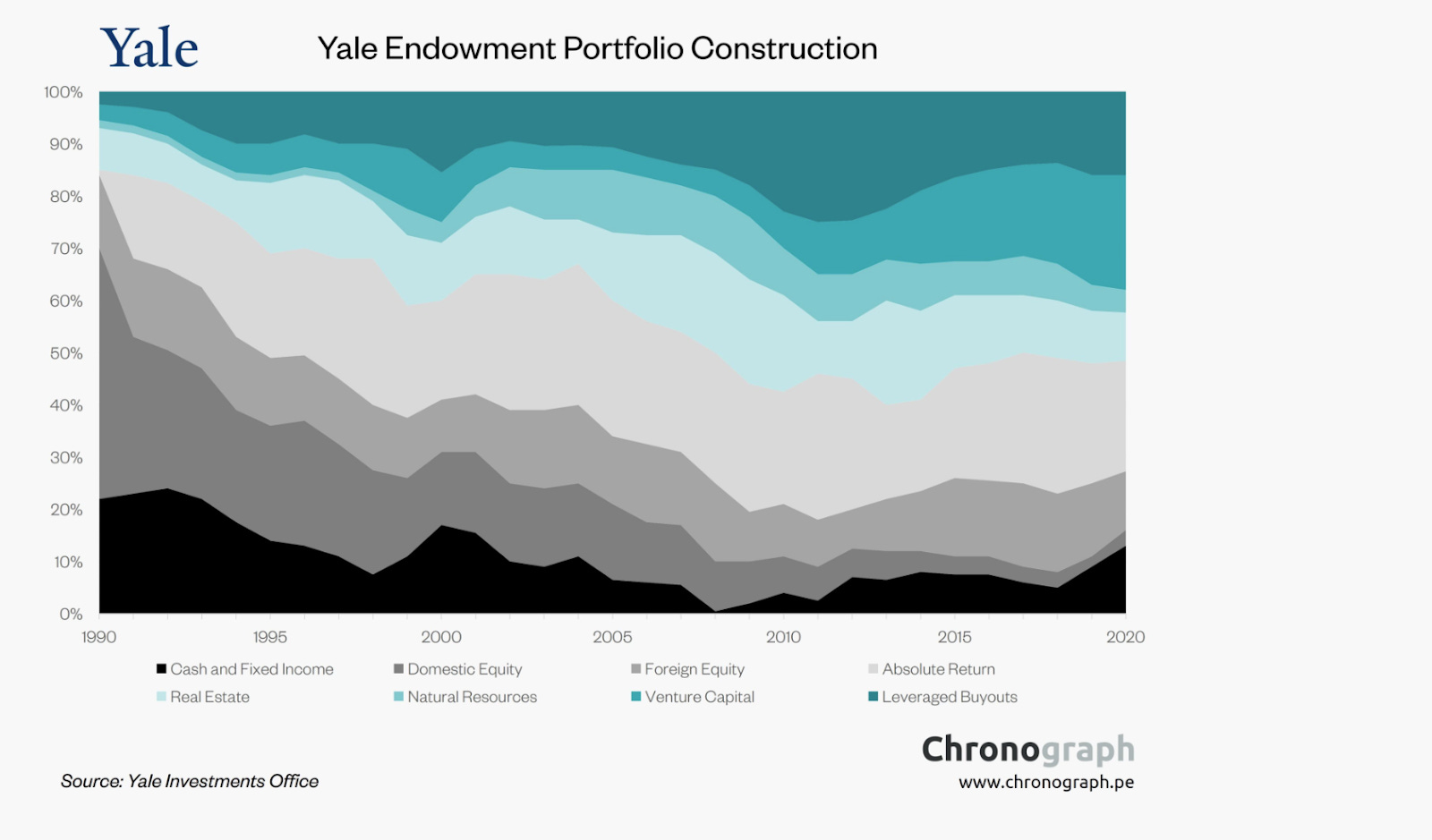

Figure 2: Yale Endowment Commitments by Fund Type

As Wendy explained to me, “Endowment-style investing is about going off the beaten path, finding strategies that are harder to execute, and then backing the people who are experts in those strategies. It’s not just about diversification, it’s maximizing returns for the risk you’re willing to take.”

That philosophy made U.S. endowments not just financial backers of universities but shapers of the venture ecosystem itself.

The Pressures on Endowments Today

Despite their reputation, endowments face real constraints. Liquidity is one of the biggest. As Wendy stated, “university endowments have been slower to deploy more capital into private investments because distributions just aren’t coming back as quickly.” With IPOs and exits lagging, many institutions have had to issue bonds or sell older fund positions on the secondary market just to free up cash (more on Cambridge Associates).

They’re also facing uncomfortable questions. In Washington, lawmakers have started asking why universities with tens of billions in their portfolios still enjoy generous tax breaks while tuition keeps climbing (more on AP News). It’s not a great look when elite schools are richer than ever, but families are going deeper into debt to send their kids there.

And then there’s the market itself. Higher interest rates and a sluggish private market have made even the top players look average. Yale, long the poster child of this model, has had years where returns barely beat a simple stock-and-bond portfolio.

As Wendy put it, all of this has made endowments more cautious, pulling back from the aggressive investing that made them famous. That hesitation is opening the door for new players, wealth managers, individuals, and funds like Ivy Invest, to step into the space they once dominated.

Why Endowments Matter for Venture Capital

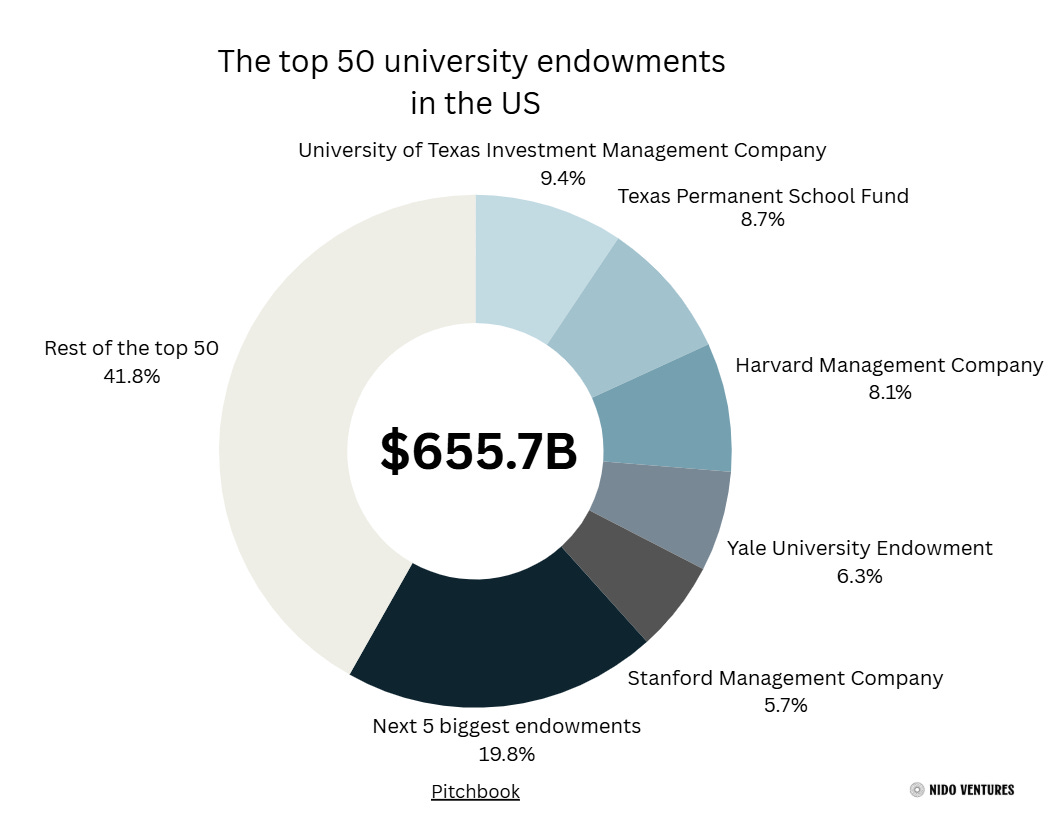

Endowments have become the backbone of venture capital because they can play the long game. Unlike most investors, they don’t need quick liquidity; their goal is to preserve and grow capital for generations. That patience makes them ideal LPs for venture, where payoffs can take a decade or more. University endowments represent 15-20% of all venture capital funding in the United States, with the top 30 endowments providing the majority of this capital (more on Forbes).

Figure 3: Concentration of the Top 50 U.S. University Endowments

It’s also a strategy that pays off. Endowments with over 30% allocated to private markets, including venture and private equity, earned a median 10-year return of 8.3%, compared to just 6.5% for those with less than 5% in private investments (more on Cambridge Associates). That willingness to back illiquid, high-risk strategies early on is what turned places like Yale and Stanford into powerhouse investors — and, by extension, what helped fuel the rise of the modern VC industry.

But it’s not just the money, it’s the quality of the capital. Endowments offer what fund managers value most: patience. They don’t face redemption pressure when markets dip, they can write extensive anchor checks, and when relationships work, they last across multiple fund vintages. On top of that, endowment teams bring a level of due diligence and professionalism that elevates the entire industry.

The Yale case shows just how powerful this can be. At one point, Yale had nearly a 28.5% target allocation to venture capital — far above the average educational institution’s 7.5% (more on Cambridge Associates). Over the decade ending in 2020, its VC bets returned an eye-popping 21.3% annually, and in 2021, those gains drove a record 40.2% overall return for the endowment (more on Yale). As Yale’s Danny Otto put it, “we view the opportunity to harness novel technologies to build new businesses across all sectors of the economy as a generational one.”

Of course, this cuts both ways. Heavy exposure to illiquid, volatile venture funds has also created drawdowns. Yale’s 2024 return of just 5.7% was the second-lowest in the Ivy League, a reminder that alternatives amplify both upside and downside (more on NEPC). And today, the model is under pressure: distributions are slow, valuations are being questioned, and many endowments are net negative on cash flows, forcing them to pace commitments more cautiously.

The Missing Piece in Latin America

If endowments are the backbone of American venture capital, in Latin America, they are nearly invisible. It’s not an issue of resources: across the region, large university and philanthropic portfolios exist, but these are usually invested conservatively or managed by private banks. As Wendy Li noted, even in the U.S., some wealthy families “just give all their money to J.P. Morgan,” in Latin America, that’s the norm.

Latin America’s university endowment scene is sparse and conservative. While a handful of institutions have formal endowment funds — such as Chile’s Pontificia Universidad Católica with $70 million — these pale in comparison to their U.S. counterparts. More importantly, they stick to traditional allocations: stocks, bonds, and fixed income, with little to no exposure to alternatives like venture capital or private equity. Where American endowments pioneered aggressive diversification into alternatives, Latin American institutions largely park their capital in conservative portfolios or hand management over to private banks.

But even for those institutions or individuals looking to access Venture Capital, entry barriers remain high. VC funds in the region typically require minimum investments of $50,000 to several million dollars (more on Latam Republic), far above what most local investors or smaller foundations can commit. Without the scale or expertise of their U.S. counterparts, many potential LPs find themselves shut out of the ecosystem. As a result, Latin American alternative assets remain concentrated in a relatively small group of family offices, fund of funds, and high-net-worth individuals, limiting both the diversity and reach of the region’s innovation funding. Ivy Invest's endowment-style fund serves as a model, requiring a minimum investment of only $1,000 for participation.

The result? Startups miss out on stable capital, and institutions forgo the long-term compounding that alternatives have delivered for peers like Yale (whose VC bets produced 21% annualized returns over a decade). In the U.S., the chain is clear: endowments commit to funds, those funds back startups, and the returns flow back to sustain the endowment. In Latin America, that link is largely missing. Bridging this gap, whether by building real endowment offices or tapping new vehicles like Ivy Invest, could unlock enormous value for both sides of the ecosystem.

Looking Ahead

The future of endowments in venture capital will depend on whether their lessons can be effectively applied. In the U.S., these funds have proven that patient, diversified capital can fuel not only university budgets but entire innovation ecosystems. Latin America has the resources to follow suit, but it will require a shift in culture, structure, and access.

For universities and foundations, the challenge is to move beyond conservative allocations and start building professional investment offices that think in decades, not quarters. For funds, the opportunity lies in finally connecting with long-term LPs who can anchor funds through cycles. And for emerging vehicles like Ivy Invest, the opening is to show that endowment-style investing doesn’t have to be limited to billion-dollar institutions; it can be adapted to smaller pools of capital and even individuals.

Special thanks to Wendy Li at Ivy Invest for her insights.

Written by

| A guest post by

|