The Atoms Strike Back

The Metrics Are Different. The Results Are Not.

The Rise of VC

Modern venture capital was born in the aftermath of World War II when Harvard professor and General Georges Doriot founded the American Research and Development Corporation (ARDC) in Boston (More on Founders Podcast). Before ARDC, the primary source of funding for new ventures was a fragmented network of angel investors. ARDC professionalized this process, raising capital from institutional sources like universities, insurance companies, and mutual funds, and channeling it into promising technologies that had gained traction during the war.

One of ARDC’s most legendary successes was its 1957 investment in Digital Equipment Corporation (DEC). The firm invested $70,000 for a 77% stake in the fledgling company. When DEC went public eleven years later, its value had soared to $355 million, delivering a staggering 500x return on ARDC’s initial investment (More on GoingVC). This landmark success story ignited the venture capital industry. In the following decades, VC funds began to appear across the United States and eventually the world, primarily financing the physical infrastructure required to support developing technology.

Why Internet Technology Became VC’s Favourite Investment

The 1990s and the dawn of the public internet marked a pivotal shift. As the digital world expanded, a new wave of companies sought venture funding, and the VC industry found its perfect match. By the 2000s, the synergy between VC and tech startups was undeniable, creating a powerful playbook for software-as-a-service (SaaS) investments that dominated the next two decades.

This model was incredibly attractive for several reasons:

High Gross Margins: Unlike industrial or hardware businesses, SaaS companies had no raw materials to procure or complex physical supply chains to manage. This allowed them to scale rapidly and efficiently.

Measurable Metrics: A new lexicon of metrics—Monthly Recurring Revenue (MRR), Lifetime Value (LTV), Customer Acquisition Cost (CAC), and Churn—emerged, allowing investors to measure growth and predict future performance with unprecedented accuracy.

Low Capital Expenditures (CapEx): The rise of cloud computing commoditized infrastructure. Suddenly, a world-changing company could be started with little more than a laptop and a subscription to a cloud server.

This new, capital-efficient model was perfectly suited for venture capital’s high-risk, high-return mandate. VCs sought ventures that could generate massive returns as quickly as possible, a dynamic that pushed sectors focused on physical products into a niche category for more specialized firms. The world of “bits” reigned supreme.

As of July 2025, there are over 1,200 unicorn companies around the world, with financial services and enterprise software dominating the landscape (More on CBInsights). Concurrently, more than 3,000 venture capital firms are active worldwide, managing assets of approximately $1.25 trillion (More on NVCA).

The Industry (Re)Awakens

History has shown that when technological, economic, and market forces align, they can trigger profound and lasting industrial transformations. Today, we are witnessing such an alignment, signaling a resurgence of interest and investment in the physical world. The atoms are striking back.

Our society has long been fascinated with robotics, a fascination amplified by pop culture. In practice, however, robots have been limited by their clunky movements and rudimentary reasoning. Their application has been confined to highly structured environments like factory floors, where they perform repetitive tasks and monitor machine systems. This represented a direct trade-off: higher initial CapEx for lower long-term operational expenditures (OpEx).

The recent explosion in AI research is poised to shatter these limitations. We are on the cusp of an era where robots can adapt to dynamic, specific tasks, impacting both CapEx and OpEx simultaneously. This potential has not gone unnoticed. Y Combinator’s recent calls for startups show a renewed and vigorous interest in hardware. AI is enabling a fundamental vision shift, creating new demand and empowering startups to elevate industry to a new level.

The opportunity is not just about reducing labor costs or layering more software onto old systems. It’s about fundamentally optimizing how new technologies are integrated into existing pipelines without entirely removing the human element. By reducing maintenance downtime and commissioning time in factories, productivity can be supercharged. As Y Combinator noted in its S25 request for startups: “Robotics hasn’t had its ChatGPT moment yet, but we think it’s almost here” (More on Y Combinator). This sentiment applies with equal force across the entire industrial sector.

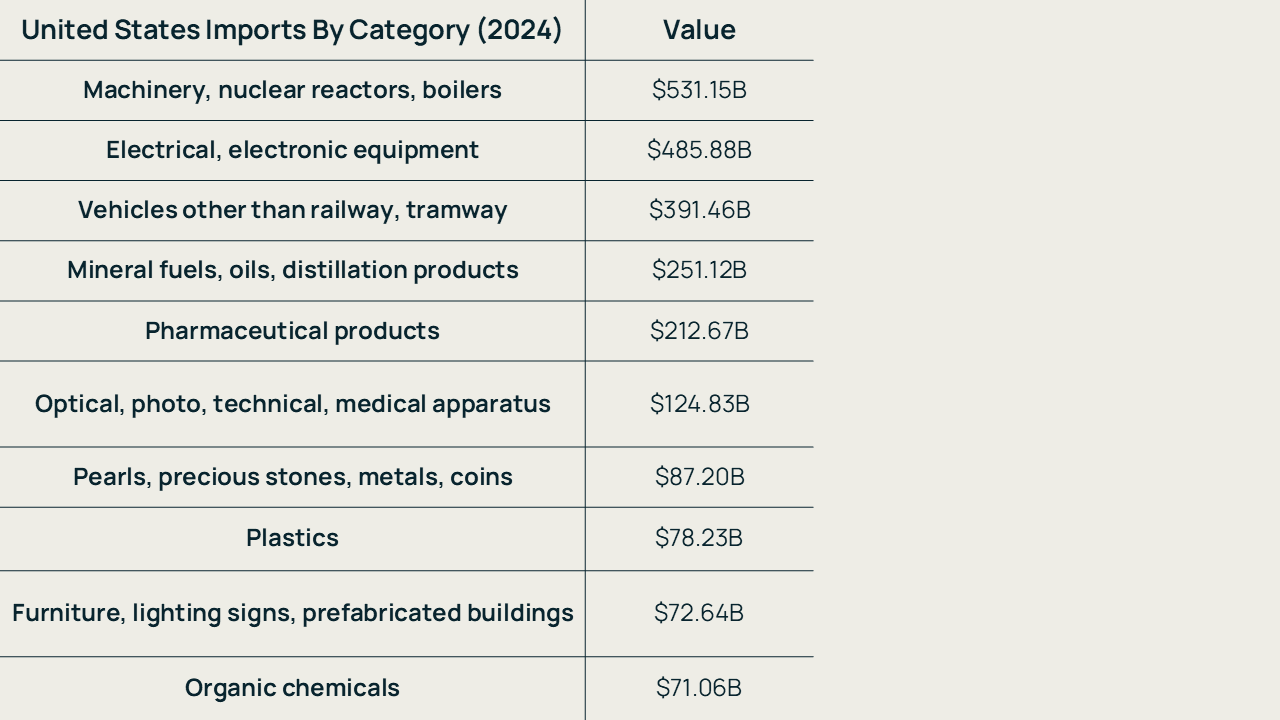

In recent years, the “return of US manufacturing” has become a familiar headline. In reality, the United States has always maintained formidable manufacturing capabilities. A look at the country’s top imports reveals a telling pattern: machinery, nuclear reactors, boilers, and electronic equipment consistently top the charts. These are not simple commodities; they are high-value, complex products often produced by large, established companies or in highly specialized, difficult-to-replicate niches.

Figure 1. US Imports by Category in 2024 (Trading Economics)

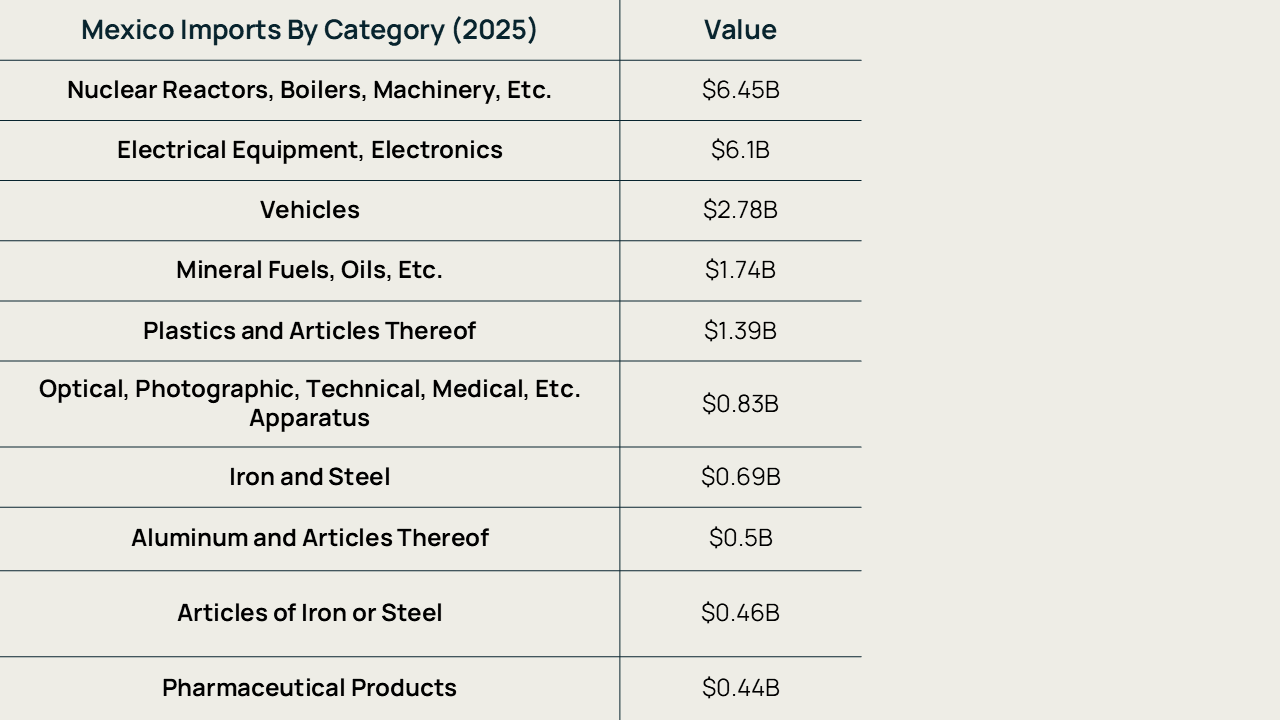

This trend holds true for Mexico’s top imports, focusing on high-value industrial and electronic goods, albeit on a smaller scale.

Figure 2. Mexico Imports by Category in 2025 (Data Mexico)

This economic landscape reveals a crucial shift. The focus is moving from creating new consumer necessities to addressing existing industrial and fiscal realities. This creates a disruptive opportunity to move away from simply creating software products and toward adopting advanced technology to build holistic, integrated products. With venture capital’s backing, a surge of companies built on this principle is likely in the coming years.

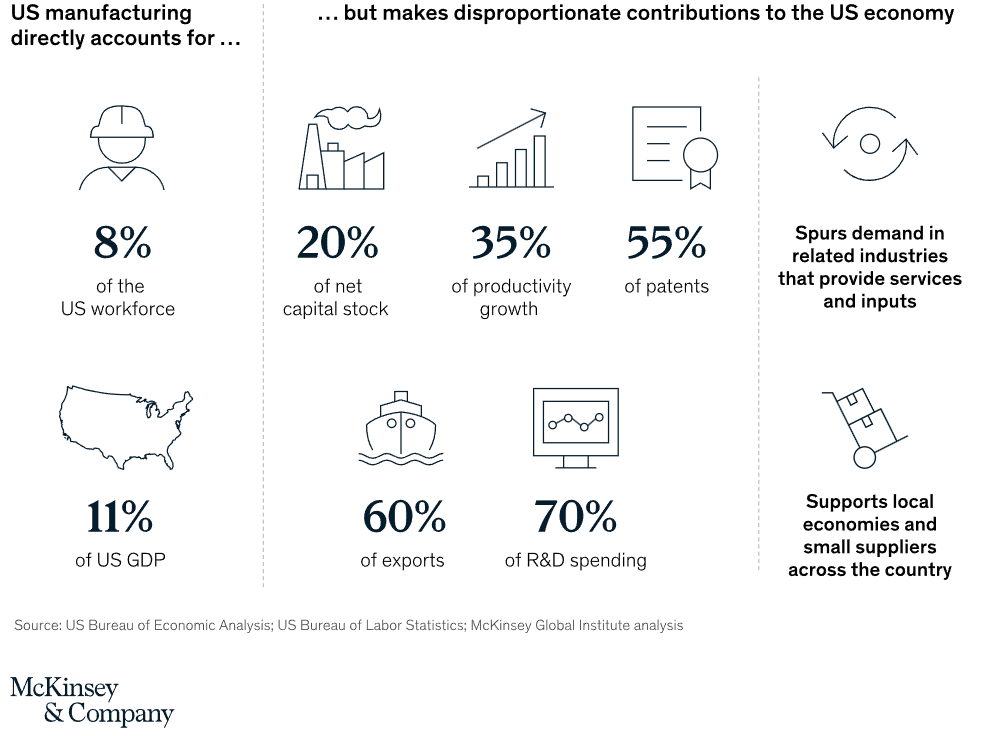

Manufacturing’s economic impact is also disproportionately large compared to its direct footprint, as highlighted by analysis from McKinsey.

Figure 3. Manufacturing creates outsize economic impact in the US (McKinsey).

Even though manufacturing directly employs around 12 million people in the US and contributes over $3.1 trillion to the GDP, its real power lies in its role as an engine for innovation. The highest intensity of R&D spending is found in sectors like pharmaceuticals, electronics, semiconductors, and medical devices. These are the fields that underpin national innovation and competitiveness. In contrast, more traditional, basic manufacturing sectors have lower R&D spending, making them ripe for disruption by new players with a different approach. As industrial-focused startups emerge, their critical differentiator will be the intelligent application of surging technologies to create solutions that are superior not only in budget but also in sustainability.

Building and investing in industrial startups is not for the faint of heart. But as the saying goes, nothing worthwhile is ever easy. The correct application of AI to optimize legacy processes that have stagnated on the manufacturing side will unlock a new generation of solutions.

However, the barriers to entry are formidable. Penetrating an industrial supply chain is a monumental obstacle, as many are built on decades-long relationships and complex offshore joint ventures. The titans of industry are where they are for a reason: they have weathered numerous economic cycles and have mastered the art of producing their products as efficiently and inexpensively as possible. While they may appear to be slow-moving incumbents in terms of technology adoption, they are survivors who have adapted time and again.

Industrial startups require more initial investment and have longer paths to profitability; they might need to reach a Series B or beyond to see positive operating numbers. Furthermore, competition is often a winner-takes-all scenario. In software, a competitor can often copy a differentiating feature, making a competitive advantage feel subjective. In industry, the advantage is objective and measurable—no one wants the second-best turbine or the second-most-efficient robotic arm, especially if the price is comparable. This creates a higher-risk, higher-reward dynamic for both the investors and the startup team. It demands stronger founders who can not only build a product but also convince an entire industry that their paradigm shift is inevitable (More on Invest Like The Best).

The founder profile is also different. In software, the average founder age is around 40, and much younger founders are common. In deep tech sectors like oil and gas or biotechnology, the average age is closer to 47. A Harvard Business Review study found that founders with at least three years of prior work experience in the same narrow industry as their startup were 85% more likely to launch a highly successful company (More on HBR). While there are people who come out of a university who can build something in consumer and build an extraordinary company, industrial startups demand a founder with a deep, nuanced understanding of the “know-how” of the product, its role in the supply chain, and the intricate dance of the market.

The adoption of AI into every sector has only just begun, and it has sent a clear message to the physical world: it’s time to keep up. Latin America, in particular, could become a fertile ground for a new generation of founders who can expertly weave together the worlds of bits and atoms. Entrepreneurs from the region are uniquely battle-tested, accustomed to navigating highly volatile markets and challenging governments. Three key factors have established a strong foundation for this industrial renaissance.

Large, successful multinational companies have established, with local companies growing exponentially, the industrial ecosystem has matured, creating world-class local teams and deep supply chain relationships. These existing networks can be pivotal for distributing and selling new industrial products.

The region is home to highly capable entrepreneurs and engineers already working in industry, who bring a potent combination of technical expertise and practical ingenuity to solve complex real world pain points of modern manufacturing. While navigating less favorable environments than the US.

Venture Capital is not new to Mexico or the LatAm region, but its accessibility and exposure has grown significantly in recent years. Growing access to funding, creating a viable and attractive funding path for experienced entrepreneurs looking to innovate within the industry.

It is a good moment to watch the founders of Latin America who are poised to build the next wave of great industrial companies. While monumental changes continue to happen in bits in Silicon Valley, the atoms are awakening to keep pace around the world.

Written by Rodrigo

| A guest post by

|

🤖🤖🤖