Secondaries 101

A Deep Dive into Latin America's Emerging Secondary Market with Attom Capital

Versión en español aquí

The venture capital landscape in Latin America is experiencing a fundamental shift as traditional exit routes remain constrained and investors seek new pathways to liquidity. At the forefront of this transformation is Antonia Rojas, Managing Partner at Attom Capital, who launched Latin America’s first dedicated direct secondaries fund in 2023. Through an in-depth conversation, Rojas provided unique insights into how secondary markets are reshaping the region’s startup ecosystem, offering a critical “oxygen” mechanism for founders, employees, and early investors while fostering long-term capital recycling that could define the next decade of Latin American entrepreneurship.

What Are Secondary Markets in Venture Capital?

Secondary transactions in venture capital represent a fundamental departure from traditional primary investments. While primary rounds inject fresh capital directly into startups to fuel growth, secondary transactions involve the purchase and sale of existing shares between investors, providing liquidity without requiring additional funding to be injected into the company. As Rojas explains, “there are two ways to partner with a company: buying primaries, where capital is used to inject growth capital, and buying from existing shareholders, the secondary, where capital is used to give oxygen to shareholders”. This distinction is crucial for understanding the benefits of the ecosystem. In primary transactions, capital serves as “gasoline” for company growth, while secondary transactions provide “oxygen” to stakeholders who have been holding illiquid positions for years. The oxygen analogy is particularly apt in Latin America, where the scarcity of exits and lengthy holding periods make secondary transactions a crucial source of liquidity for investors, unlike in mature markets such as the United States, where exits occur more frequently and predictably (more on CuanticoVC and BuenTrip Ventures).

The secondary market encompasses two primary transaction types: direct secondaries, where investors purchase shares directly in specific companies, and indirect secondaries, where investors buy stakes in funds that hold portfolios of companies. Attom Capital focuses exclusively on direct secondaries, positioning itself as active value-add investors rather than passive financial intermediaries. “Once we partner with companies, we help them with business development, talent, growth—our only difference with a traditional VC is how we enter the companies,” Rojas noted.

Global Secondary Markets: The US and European Landscape

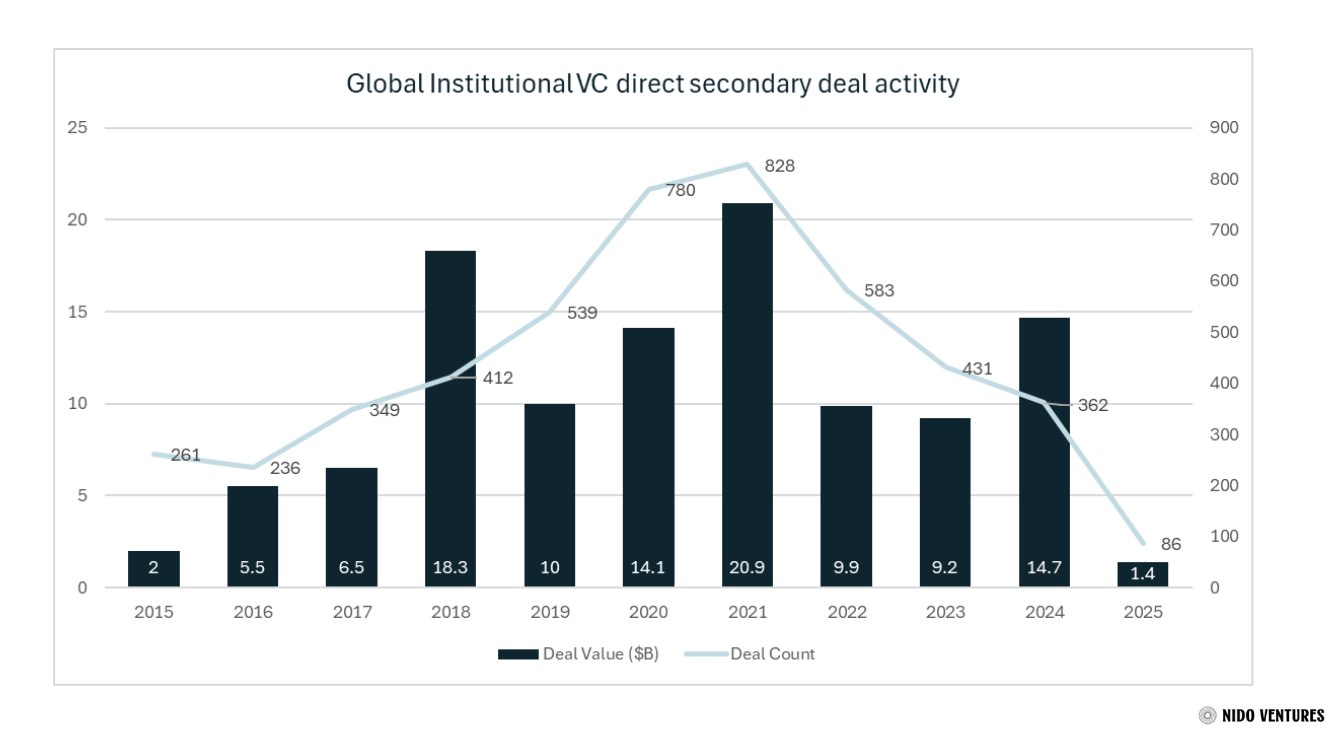

The global venture capital secondary market has experienced remarkable growth, driven by extended holding periods and constrained exit environments. Globally, direct secondaries have grown substantially, rising from 1.3% of exit value in 2021 to 4.2% in 2024. This growth reflects increasing demand for liquidity solutions as traditional exit routes remain constrained across mature markets. In the United States, the secondary market reached an estimated $61.1 billion in annual transaction volume as of Q2 2025, representing a 22.2% increase from Q4 2024 (more on Pitchbook). Despite this substantial size, the market remains modest relative to overall venture capital needs, comprising only 1.9% of total unicorn value and 31.8% of trailing twelve-month primary VC exit value.

Figure 1: Global institutional VC direct secondary deal activity by year, showing annual deal value (in billions USD) and deal count from 2015 to 2025, highlighting peak volumes in 2021 and the significant decline in both deal value and count by 2025 (more on Pitchbook).

The US market exhibits significant concentration, with the top 15 companies accounting for 61% of the secondary market volume in 2024. This concentration reflects the information asymmetries that plague secondary investing, where investors tend to focus on recognizable, headline-grabbing names, where pricing transparency and due diligence are more feasible. Companies in high-growth sectors, such as artificial intelligence, command particular attention, with AI startups accounting for 64.1% of primary deal value, despite representing only 35.6% of the deal count (more on Pitchbook).

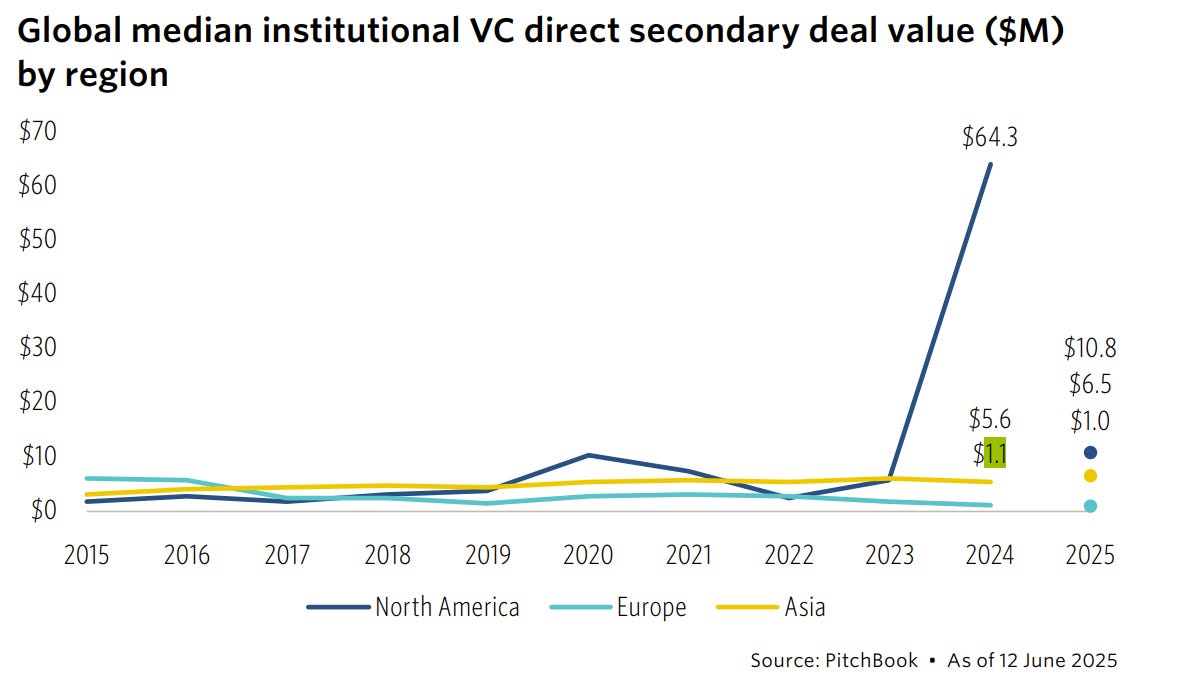

In Europe, secondary markets present a distinct dynamic, with an estimated potential market size of $47.5 billion in the base case scenario, equivalent to 7% of the aggregate market capitalization of companies valued at over $500 million. However, actual transaction activity has been significantly lower, with only $10.7 billion in institutional VC direct secondaries transacted over the past decade (more on Pitchbook).

Figure 2: Median VC direct secondary deal values by region from 2015 to 2025, showing a sharp North American spike in 2024.

Latin America’s Secondary Market: Long Liquidity Cycles and the Rappi Case

Despite Latin America’s growing startup ecosystem, the region remains drastically underrepresented in the global VC secondaries market. Only 0.73% of global VC secondaries resources were actually invested in Latin America, a disparity that highlights just how much the region lags behind North America and Europe in providing liquidity options for founders and early investors (more on Paramo Partners’ Substack).

LATAM’s venture capital ecosystem faces unique challenges that make secondary markets particularly valuable yet underdeveloped. The region’s startup landscape has grown substantially, with $4.5 billion deployed across 751 transactions in 2024 (more on LAVCA). However, this growth occurs against severely constrained exit activity, with only 79 exits recorded among VC-backed companies—the lowest level in recent years (more on Startuplinks).

The liquidity challenge manifests in extended fundraising cycles, with startups taking an average of 20 months to advance to their next funding round (more on LAVCA). As Rojas mentioned in our conversation, “Holding periods have become much longer. In the past, a company might have been acquired within five years; now, the larger and more successful ones often take ten or more years. That is why it is healthy to create intermediate stages of liquidity.” This timeline reflects both investor selectivity and the capital-constrained environment characterizing much of Latin America’s venture ecosystem.

Rappi, Colombia’s delivery giant valued at over $5.25 billion, exemplifies the region’s extended liquidity timelines. Despite being IPO-ready since 2023, Rappi’s path to public markets has been repeatedly delayed. Co-founder Simón Borrero stated in September 2024 that while the company could be “ready for IPO in 12 months,” they remain “patient” given their profitability (more on Reuters). This extended pre-IPO phase, now spanning over two years, illustrates how even Latin America’s most successful startups face prolonged liquidity cycles. Rappi has completed multiple secondary transactions, including a $150 million secondary round in January 2022, as well as additional undisclosed transactions throughout the year. These transactions allow stakeholders to realize partial returns without requiring the company to go public in unfavorable market conditions, demonstrating the critical role secondaries play in managing extended exit timelines (more on Clay).

The broader Latin American secondary market remains nascent but shows significant growth potential. The current market size is estimated at less than 1% of regional VC activity, which is notably below the 1.9% benchmark in the United States and the 7% potential in Europe. Industry projections suggest the secondary market could grow at 60% annually, driven by acute liquidity needs and ecosystem maturation (more on Reuters).

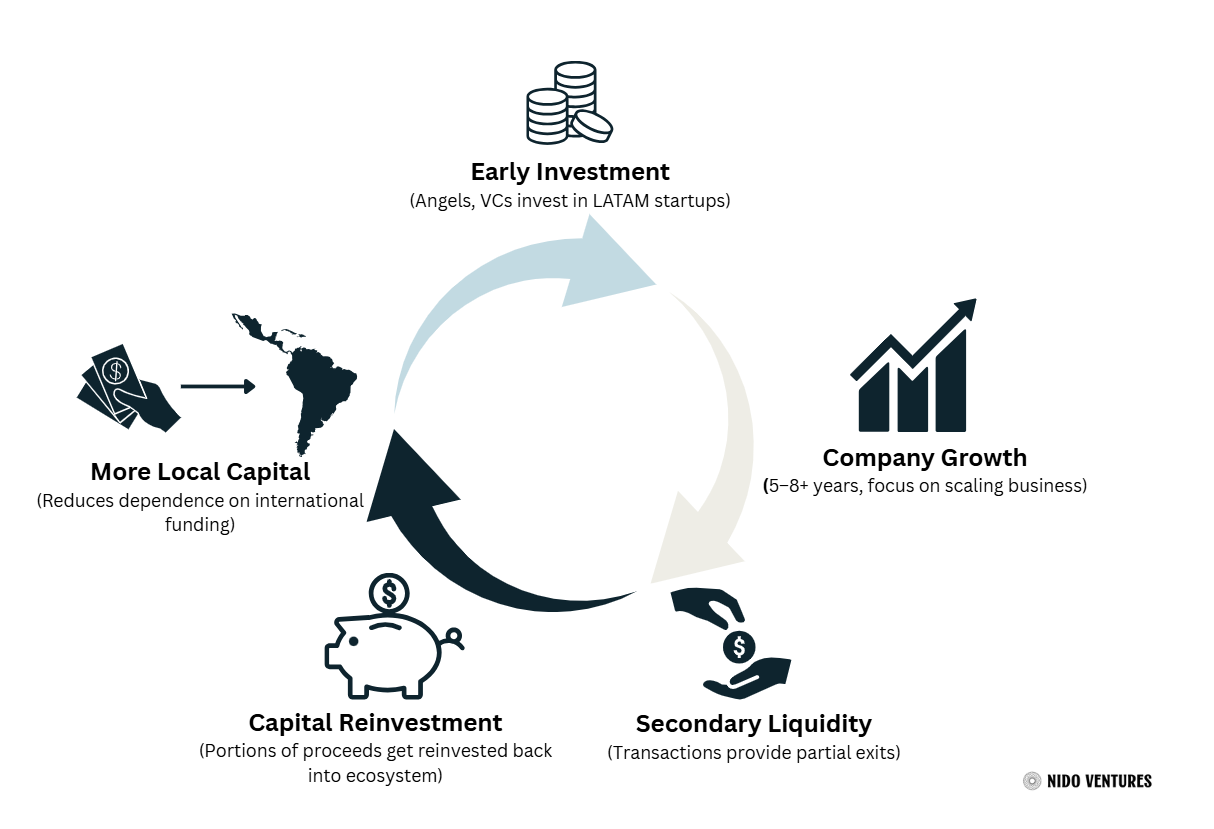

Figure 3: Capital recycling cycle in LATAM venture capital, illustrating how early investment, company growth, secondary liquidity, and reinvestment lead to more local capital and a stronger ecosystem.

Attom Capital: Pioneering Direct Secondaries in Latin America

Attom Capital emerged as a response to the critical lack of liquidity options for founders and early investors throughout the region. Rojas saw firsthand, through her experience as an angel investor and Limited Partner (LP), how illiquid positions constrained both personal and ecosystem growth. “I started selling my angel positions in secondaries,” and said, “This is tremendous, how can there not be a fund specializing in this?” she recalls. Attom focuses on direct secondaries and acts as an active partner, providing business development, talent support, and growth expertise, not simply financial liquidity. They keep founders motivated: secondaries are typically for “much less than 10%” of holdings, ensuring founders remain incentivized for long-term growth.

Sector focus at Attom includes fintech and B2B SaaS, with flexibility across the region, provided there’s an operational foothold in Mexico or Brazil, key hubs for scalability. Their relationships are built over time, “we like to know companies at least two years before investing,” Rojas says, reflecting rigor and trust. Attom’s seven-year fund life is shorter than the standard VC, as it invests at growth stages where exits, although still delayed, are more readily visible.

Market Outlook

Based on our conversation with Rojas, Latin America’s secondary activity is poised for significant expansion, especially as the ecosystem matures and liquidity remains a major challenge. Rojas stresses that “the importance of education is vital, so people actually understand what we’re doing,” noting that misconceptions around secondaries can slow healthy market development. She highlights that roughly “the majority of capital that gets unlocked through secondaries ends up being reinvested in local startups,” creating a virtuous cycle that reduces reliance on foreign capital, while boosting regional innovation.

As more founders become knowledgeable about secondary market transactions, Rojas recommends they “do diligence on secondary investors, exactly as they would with a primary VC,” to protect governance and the long-term health of their cap tables. She emphasizes, “a secondary investor is not just extra liquidity, it’s someone you’ll be running with for years, it’s closer than a marriage in some cases.”

Looking forward, Rojas is optimistic but cautious, “In five or ten years, I want secondary markets in LATAM to be normalized, but done in an orderly, responsible, and value-adding way.” The region’s rapid growth will depend on continued founder education, strong governance, and building trust between investors and entrepreneurs, ensuring secondary transactions accelerate, not destabilize, ecosystem advancement. Well-structured secondaries should empower more founders to innovate, help VCs recycle capital, and strengthen overall startup resilience in Latin America.

Looking Ahead

VC secondaries are helping to correct Latin America’s liquidity imbalance. With local leaders, such as Attom Capital, the region is evolving toward faster capital rotation, better outcomes for founders, and a more resilient ecosystem. According to Rojas, responsible expansion and continued education are essential to ensure that liquidity does not compromise governance or long-term value. As secondary markets normalize, Latin America’s investors and founders will be better equipped to recycle capital, innovate, and build enduring companies for the future.

Special thanks to Antonia Rojas for her valuable time, insights, and contributions that were central to this deep dive.

Written by Roberto Mazariegos

| A guest post by

|